COSO Committee of Sponsoring Organizations of the Treadway Commission

Committee of Sponsoring Organizations of the Treadway Commission

| Prev | Next | |

This publication, Internal Control—Integrated Framework: Illustrative Tools for Assessing Effectiveness of a System of Internal Control (Illustrative Tools), is intended to assist management when using the updated COSO Internal Control—Integrated Framework (Framework) to assess the effectiveness of its system of internal control based on the requirements set forth therein. An effective system of internal control provides reasonable assurance of achievement of an entity's objectives, relating to operations, reporting, and compliance. An effective system of internal control reduces, to an acceptable level, the risk of not achieving an objective relating to one, two, or all three categories of objectives. Accordingly, Illustrative Tools can help management to assess whether a system of internal control meets the following requirements:

-

Each of the five components and relevant principles is present and functioning; and

-

The five components are operating together in an integrated manner.

Please refer to the Framework when using Illustrative Tools. In particular, Chapter 2, Objectives, Components, and Principles, sets out the direct relationships that exist between the objectives, which are what an entity strives to achieve, and the components, which represent what is required to achieve the objectives, and relevant principles that represent fundamental concepts associated with components. Also, Chapter 3, Effective Internal Control, sets out the requirements for effective internal control and the criteria, relevant for the objective category, for classifying the severity of any internal control deficiencies.

This publication is organized into two fundamental sections: Templates and Scenarios.

-

The templates can support an assessment of the effectiveness of a system of internal control and help to document such an assessment.

-

The scenarios illustrate several practical examples of how the templates can be used to support an assessment of effectiveness of a system of internal control.

The templates and scenarios focus on evaluating components and relevant principles, not the underlying controls (e.g., transaction-level control activities) that affect the relevant principles. These tools are not designed to satisfy any criteria established through laws, rules, regulations, or external standards for evaluating the severity of internal control deficiencies associated with a particular entity objective, such as external financial reporting. As noted in the Framework, when regulators, standard-setting bodies, and other relevant third parties establish criteria for defining the severity of, evaluating, and reporting internal control deficiencies, management should use only those criteria.

The templates are designed to present only a summary of assessment results. They are not an integral part of the Framework, and they may not address all matters that need to be considered when assessing a system of internal control. Further, they do not represent a preferred method of conducting and documenting an assessment. Their purpose is limited to illustrating one possible assessment process based on the requirements for effective internal control, as set forth in the Framework.

The templates do not illustrate management's selection and deployment of controls to effect principles or its determination of scope, nature, timing, and extent of evaluating such controls embedded within the components. The facts and circumstances relevant to an assessment vary among different categories of objectives and among different entities and industries; therefore, the practical use of these tools also varies.

As the Framework applies to any type of entity—large and small public, private, governmental, and not-for-profit—so do the templates. Management can modify the templates to reflect unique facts and circumstances (e.g., specified objectives and sub-objectives, scope of application, organizational structure) and assessment processes for the entity. For example:

-

An entity with a complex organizational structure can modify or supplement the templates appropriately, as illustrated in Scenario E: How are the assessments of multiple locations combined?

-

A smaller entity can simplify the templates to reflect a less complex organizational structure and to acknowledge a less formal, less structured system of internal control; for instance a system that reflects more direct supervision and continuous communication about internal control among the CEO, senior managers, and other personnel.

-

An entity may use technology to maintain a summary of internal control deficiencies that is referenced by all the templates rather than having summaries included in each template.

Organizations may leverage the templates to develop or configure technology-based solutions to support separate and/or ongoing evaluations and assessment processes. Technology-based solutions, ranging from a simple spreadsheet to sophisticated, enterprise-wide application software, can help the organization document and monitor the entity's controls and management's effectiveness assessment. Technology-based solutions can provide relevant information through system-generated reports and dashboards, which in turn may be used by stakeholders such as owners, a board of directors, fn 1 senior management, operating unit and functional managers, control and compliance personnel, and auditors. Management considers the outputs of the technology-based solutions to support its assessment of a system of internal control, but management would generally exercise judgment about its overall assessment outside of its technology-based solution.

Organizations can customize the level and amount of detail included in the templates, as they deem necessary. For example, consider Principle 2, Exercises Oversight Responsibility. Controls that effect this principle likely occur at the entity level, and management may determine that documentation relating to these controls may not need to be extensive to support the evaluation. Accordingly, in this example, the templates can be used to fully document and assess whether this relevant principle is present and functioning. In contrast, controls to effect Principle 10, Selects and Develops Control Activities are likely deployed in many business processes throughout the organization and, accordingly, documentation relating to these controls would be expected to be more extensive and detailed. Documentation of management's evaluation of whether this principle is present and functioning would likely require additional templates, such as detailed risk and control matrices, which are not set forth in Illustrative Tools.

In summary, management may use these templates in several important ways:

-

To help determine whether all five components of a system of internal control are operating together in an integrated manner

-

To help determine whether components and relevant principles are present and functioning

-

To help assess whether the system of internal control is effective relating to one category of objectives, such as reporting, or more than one category

-

To document management's assessment relating to the effectiveness of a system of internal control at the entity and subunit levels, considering components and relevant principles

-

To document internal control deficiencies identified during the assessment process

If the templates are used as suggested, they:

-

Provide a logical structure for management to analyze and document the organization's assessment of effectiveness of internal control, including the presence and functioning of components and relevant principles as set forth in the Framework

-

Assist management in developing a process for identifying and evaluating internal control deficiencies within components and relevant principles relating to its assessment of effectiveness of internal control

To assist management in assessing whether a system of internal control reduces to an acceptable level the risk of not achieving an objective, the templates are organized to support a risk-based assessment approach. Four different templates are included: fn 2

-

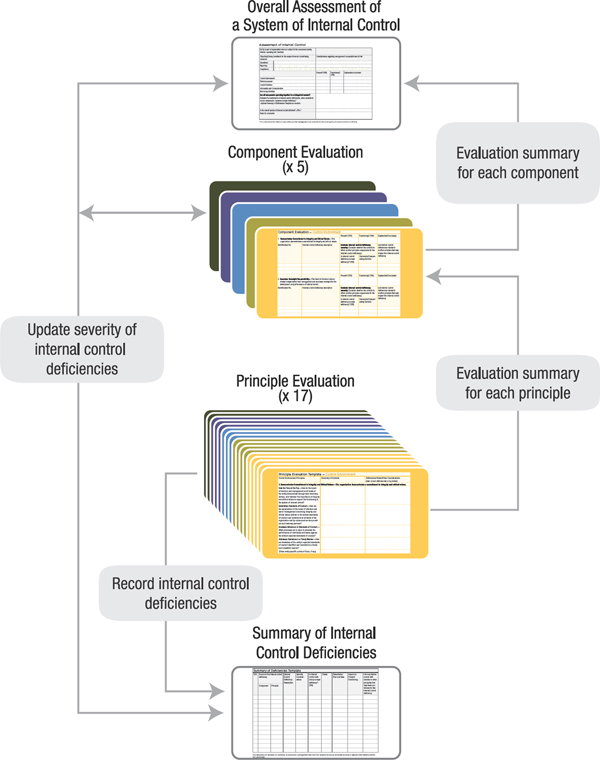

Overall Assessment of a System of Internal Control—Summarizes management's determination of whether each of the components and relevant principles is present and functioning and components are operating together in an integrated manner, including the severity of internal control deficiencies or combination of deficiencies when aggregated across the components.

-

Component Evaluation—Summarizes management's determination of whether each component and relevant principles are present and functioning. Internal control deficiencies relating to a principle are listed and the severity of each deficiency is assessed considering compensating controls fn 3 (whether or not associated with that particular component or principle).

-

Principle Evaluation—Summarizes management's determination of whether each relevant principle is present and functioning. fn 4 Management considers controls in conjunction with its assessment of components and relevant principles. The Framework does not prescribe specific controls that must be selected, developed, and deployed for an effective system of internal control. That determination is a function of management judgment based on factors unique to each entity. The absence of controls necessary to effect relevant principles would represent an internal control deficiency.

The Framework allows for judgment in assessing the potential impact of a deficiency on the presence and functioning of a relevant principle. Management may consider other controls (whether or not associated with that particular component or principle) that compensate for an internal control deficiency. These templates also summarize any identified internal control deficiencies along with a preliminary determination of the severity of the internal control deficiencies. The determination of severity is preliminary pending the consideration of whether there are any compensating controls.

The Framework describes points of focus that are important characteristics of principles. The points of focus may assist management in assessing whether relevant principles are, in fact, present and functioning. The Framework does not require that management assess separately whether points of focus are in place. Points of focus are provided in Illustrative Tools as useful references.

-

Summary of Internal Control Deficiencies—A log of all identified internal control deficiencies that can be leveraged in the evaluation of components and principles, and can enable the internal control deficiencies to be aggregated.

The diagram above shows the relationship between each of the templates and the expected flow of key information (i.e., evaluation summaries and internal control deficiencies). An assessment process, as reflected in the templates, would likely proceed as follows:

1. Principle evaluation—Considering the controls to effect the principle. Internal control deficiencies would be identified along with an initial severity determination.

2. Component evaluation—Considering the roll up of the results of the component's principle evaluations. The severity of internal control deficiencies is re-evaluated considering whether controls to effect other principles within and across components compensate for the deficiency.

3. Assessment of the effectiveness of internal control—Considering the roll up of the results of the component evaluations and assessing whether the components are operating together in an integrated manner by evaluating whether any internal control deficiencies aggregate to a major deficiency.

As economic, industry, and regulatory environments change, the scope and nature of an entity's leadership, priorities, business model, organization, business processes, and activities need to adapt and evolve. Internal control effective within one set of conditions may not necessarily be effective when those conditions change significantly. As part of risk assessment, management identifies changes that could significantly impact the entity's system of internal control and takes action as necessary. Accordingly, after an initial assessment, management continually assesses the effectiveness of the system of internal control, and while the process is depicted here as serial, in practice it is likely to be iterative.

fn 1 As in the Framework, the term "board of directors" is used in this publication to encompass the governing body, including board, board of trustees, general partners, owner, or supervisory board.

fn 2 For illustrative purposes the templates are shown as separate documents. In practice, an organization would likely use technology to link these templates to reduce redundant information; information common to more than one template would then automatically be populated across the templates. For example, an organization will likely use technology to maintain a summary of internal control deficiencies that is referenced by all the templates rather than having summaries included in each template.

fn 3 This publication broadly uses the term "compensating controls" as defined by the Securities Exchange Commission in the United States: "Compensating controls are controls that serve to accomplish the objective of another control that did not function properly, helping to reduce risk to an acceptable level."

| Prev | Up | Next |

| Home | ||

Copyright © 2013 – 2016 Committee of Sponsoring Organizations of the Treadway Commission and the American Accounting Association. All Rights Reserved. Use of materials is subject to COSO's Policy of Acceptable Use.

To access this page, please login with your COSO credentials using the button below:

Login to COSOPlease enter your COSO login credentials below

Please contact marybeth.gripshover@aaahq.org with any questions