COSO Committee of Sponsoring Organizations of the Treadway Commission

Committee of Sponsoring Organizations of the Treadway Commission

| Prev | Next | |

An organization adopts a mission and vision, sets strategies, establishes objectives it wants to achieve, and formulates plans for achieving them. Objectives may be set for an entity as a whole or be targeted to specific activities within the entity. Though many objectives are specific to a particular entity, some are widely shared. For example, objectives common to most entities are sustaining organizational success, reporting to stakeholders, recruiting and retaining motivated and competent employees, achieving and maintaining a positive reputation, and complying with laws and regulations.

Supporting the organization in its efforts to achieve objectives are five components of internal control:

-

Control Environment

-

Risk Assessment

-

Control Activities

-

Information and Communication

-

Monitoring Activities

These components are relevant to an entire entity and to the entity level, its subsidiaries, divisions, or any of its individual operating units, functions, or other subsets of the entity.

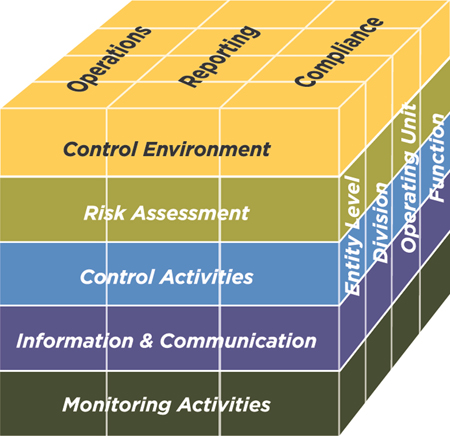

A direct relationship exists between objectives, which are what an entity strives to achieve, components, which represent what is required to achieve the objectives, and entity structure (the operating units, legal entities, and other structures). The relationship can be depicted in the form of a cube.

-

The three categories of objectives are represented by the columns.

-

The five components are represented by the rows.

-

The entity structure, which represents the overall entity, divisions, subsidiaries, operating units, or functions, including business processes such as sales, purchasing, production, and marketing and to which internal control relates, are depicted by the third dimension of the cube. fn 3

Each component cuts across and applies to all three categories of objectives. For example, attracting, developing, and retaining competent people who are able to conduct internal control—part of the control environment component—is relevant to all three objectives categories.

The three categories of objectives are not parts or units of the entity. For instance, operations objectives relate to the efficiency and effectiveness of operations, not specific operating units or functions such as sales, marketing, procurement, or human resources.

Accordingly, when considering the category of objectives related to reporting, for example, knowledge of a wide array of information about the entity's operations is needed. In that case, focus is on the middle column of the model—reporting objectives—rather than on the operations objectives category.

Internal control is a dynamic, iterative, and integrated process. For example, risk assessment not only influences the control environment and control activities, but also may highlight a need to reconsider the entity's requirements for information and communication, or for its monitoring activities. Thus, internal control is not a linear process where one component affects only the next. It is an integrated process in which components can and will impact another.

No two entities will, or should, have the same system of internal control. Entities, objectives, and systems of internal control differ by industry and regulatory environment, as well as by internal considerations such as the size, nature of the management operating model, tolerance for risk, reliance on technology, and competence and number of personnel. Thus, while all entities require each of the components to maintain effective internal control over their activities, one entity's system of internal control will look different from another's.

fn 3 Throughout the Framework, the term "the entity and its subunits" refers collectively to the overall entity, divisions, subsidiaries, operating units, and functions.

| Prev | Up | Next |

| Home | ||

Copyright © 2013 – 2016 Committee of Sponsoring Organizations of the Treadway Commission and the American Accounting Association. All Rights Reserved. Use of materials is subject to COSO's Policy of Acceptable Use.

To access this page, please login with your COSO credentials using the button below:

Login to COSOPlease enter your COSO login credentials below

Please contact marybeth.gripshover@aaahq.org with any questions