COSO Committee of Sponsoring Organizations of the Treadway Commission

Committee of Sponsoring Organizations of the Treadway Commission

| Prev | Next | |

Chapter Summary

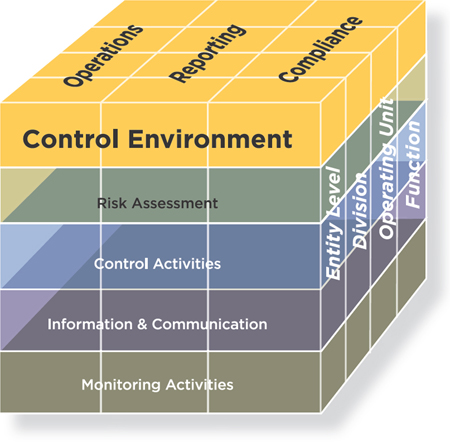

The control environment is the set of standards, processes, and structures that provide the basis for carrying out internal control across the organization. The board of directors and senior management establish the tone at the top regarding the importance of internal control including expected standards of conduct. Management reinforces expectations at the various levels of the organization. The control environment comprises the integrity and ethical values of the organization; the parameters enabling the board of directors to carry out its oversight responsibilities; the organizational structure and assignment of authority and responsibility; the process for attracting, developing, and retaining competent individuals; and the rigor around performance measures, incentives, and rewards to drive accountability for performance. The resulting control environment has a pervasive impact on the overall system of internal control.

Principles relating to the Control Environment component

1. The organization demonstrates a commitment to integrity and ethical values.

2. The board of directors demonstrates independence from management and exercises oversight of the development and performance of internal control.

3. Management establishes, with board oversight, structures, reporting lines, and appropriate authorities and responsibilities in the pursuit of objectives.

4. The organization demonstrates a commitment to attract, develop, and retain competent individuals in alignment with objectives.

5. The organization holds individuals accountable for their internal control responsibilities in the pursuit of objectives.

The control environment is influenced by a variety of internal and external factors, including the entity's history, values, market, and the competitive and regulatory landscape. It is defined by the standards, processes, and structures that guide people at all levels in carrying out their responsibilities for internal control and making decisions. It creates the discipline that supports the assessment of risks to the achievement of the entity's objectives, performance of control activities, use of information and communication systems, and conduct of monitoring activities.

An organization that establishes and maintains a strong control environment positions itself to be more resilient in the face of internal and external pressures. It does this by demonstrating behavior consistent with the organization's commitment to integrity and ethical values, adequate oversight processes and structures, organizational design that enables the achievement of the entity's objectives with appropriate assignment of authority and responsibility, a high degree of competence, and a strong sense of accountability for the achievement of objectives.

Organizational culture supports the control environment insofar as it sets expectations of behavior that reflects a commitment to integrity and ethical values, oversight, accountability, and performance evaluation. Establishing a strong culture considers, for example, how clearly and consistently ethical and behavioral standards are communicated and reinforced in practice. As such, culture is part of an organization's control environment, but also encompasses elements of other components of internal control, such as policies and procedures, ease of access to information, and responsiveness to results of monitoring activities. Therefore culture is influenced by the control environment and other components of internal control, and vice versa.

| Prev | Up | Next |

| Home | ||

Copyright © 2013 – 2016 Committee of Sponsoring Organizations of the Treadway Commission and the American Accounting Association. All Rights Reserved. Use of materials is subject to COSO's Policy of Acceptable Use.

To access this page, please login with your COSO credentials using the button below:

Login to COSOPlease enter your COSO login credentials below

Please contact marybeth.gripshover@aaahq.org with any questions