SET Newsletter

Hello SET Section members!

I am currently gathering items for the Summer Section Newsletter, so please let me know if you have any contributions. I would like to share information on:

- Stories and Pictures from the Midwinter Meeting

- Calls for Papers

- Teaching Tips or Resources

- Member Profiles (remember I want to emphasize fun items more than CV items)

- Any other topics you think would be interesting to fellow SET members.

Please send your contributions to Dawna Drum at dawna.drum@wwu.edu by Thursday June 18.

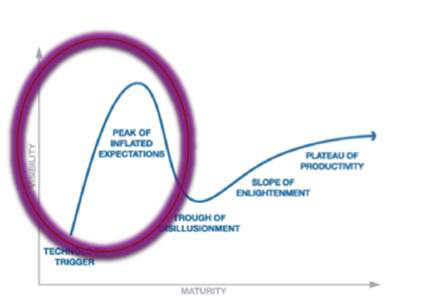

Value Proposition

The SET Section members typically follow unique approaches as to how they explore, research and teach the impact and influences of information technologies in their early stages on accounting, auditing and taxation. The following diagram may be a useful illustration. It outlines the "Hype Cycle" - a well established tool created by Jackie Fenn of the Gartner Group in 1995 that illustrates the typical business technology adoption lifecycle. The circled area is of particular interest to SET Section members.

Source: The Gartner Group

A hype cycle is comprised of five steps:

- TECHNOLOGY TRIGGER

The first phase of a Hype Cycle is the "technology trigger" where research generates innovations that couple breakthrough technologies with perceived market opportunities to generate significant press and commercial interest. New innovations all start here.

- PEAK OF INFLATED EXPECTATIONS

In the next phase, a frenzy of publicity typically expands the enthusiasm and often leads to unrealistic expectations being cited for the technology.

- TROUGH OF DISILLUSIONMENT

Technologies enter the "trough of disillusionment" because they fail to meet the overly high expectations and become unfashionable. Some innovations never get beyond this stage and disappear entirely.

- SLOPE OF ENLIGHTENMENT

Although the press may have largely stopped covering the technology, some businesses continue through the "slope of enlightenment" and experiment to understand the benefits and practical application of the technology that will have lasting impact.

- PLATEAU OF PRODUCTIVITY

A technology reaches the "plateau of productivity" as the benefits of it become widely demonstrated and accepted. The technology becomes increasingly stable and evolves into second and subsequent generations. The final height of the plateau varies according to whether the technology is broadly applicable or benefits only a niche market.

Applying this diagram to the AAA technology-focused Sections:

The SET Section researchers typically research technologies before they enter the Technology Trigger stage, or at the early stages of the Hype Cycle. Such research generates new ideas on how technologies can be effectively exploited in the accounting domain. The research is frequently exploratory in nature and often employs design science methodologies. This exploration generally occurs up to the Peak of Inflated Expectations stage - where the success and even usefulness of new technologies and ideas is still uncertain.

In comparison, the AIS Section members are interested in research across the entire technology life cycle, but are generally most active in exploring accounting technologies once the slope of enlightenment in a technology's life cycle is reached and implementation of technologies are commencing and need to be understood. AIS Section members also explore information systems issues that are not directly related to technology.

For each new technology development the research potential across all areas of the hype cycle is significant. The combined work of the AIS and SET Sections ensures that the AAA members are kept at the leading edge of research as new technologies move along this cycle.

The above Value Proposition for the SET section of the American Accounting Association was developed in conjunction with the Information Systems Section of the American Accounting Association. Find out further details of this section at http://aaahq.org/infosys/index.cfm.

Interested in technology in accounting, auditing and/or taxation?

Why not join today?

The SET Section welcomes new members who are interested in the potential role and impact of strategic and emerging technologies on all aspects of accounting, auditing and/or taxation. The group particularly welcomes joint membership from members of other AAA sections who are interested in technology aspects of another Section’s focus.

We are a dynamic group that shares a common interest in exploring emerging technologies in the accounting domain, reporting on what we find with academic rigor, discussing it with colleagues and teaching about it to our students. We'd very much welcome those sharing similar interests to join.

To illustrate the diversity of the section, the brief profile details of Section members show how these formal statements are enacted in practice.

Value Proposition

The SET Section members typically follow unique approaches as to how they explore, research and teach the impact and influences of information technologies in their early stages on accounting, auditing and taxation. The following diagram may be a useful illustration. It outlines the "Hype Cycle" - a well established tool created by Jackie Fenn of the Gartner Group in 1995 that illustrates the typical business technology adoption lifecycle. The circled area is of particular interest to SET Section members.

Source: The Gartner Group

A hype cycle is comprised of five steps:

- TECHNOLOGY TRIGGER

The first phase of a Hype Cycle is the "technology trigger" where research generates innovations that couple breakthrough technologies with perceived market opportunities to generate significant press and commercial interest. New innovations all start here.

- PEAK OF INFLATED EXPECTATIONS

In the next phase, a frenzy of publicity typically expands the enthusiasm and often leads to unrealistic expectations being cited for the technology.

- TROUGH OF DISILLUSIONMENT

Technologies enter the "trough of disillusionment" because they fail to meet the overly high expectations and become unfashionable. Some innovations never get beyond this stage and disappear entirely.

- SLOPE OF ENLIGHTENMENT

Although the press may have largely stopped covering the technology, some businesses continue through the "slope of enlightenment" and experiment to understand the benefits and practical application of the technology that will have lasting impact.

- PLATEAU OF PRODUCTIVITY

A technology reaches the "plateau of productivity" as the benefits of it become widely demonstrated and accepted. The technology becomes increasingly stable and evolves into second and subsequent generations. The final height of the plateau varies according to whether the technology is broadly applicable or benefits only a niche market.

Applying this diagram to the AAA technology-focused Sections:

The SET Section researchers typically research technologies before they enter the Technology Trigger stage, or at the early stages of the Hype Cycle. Such research generates new ideas on how technologies can be effectively exploited in the accounting domain. The research is frequently exploratory in nature and often employs design science methodologies. This exploration generally occurs up to the Peak of Inflated Expectations stage - where the success and even usefulness of new technologies and ideas is still uncertain.

In comparison, the AIS Section members are interested in research across the entire technology life cycle, but are generally most active in exploring accounting technologies once the slope of enlightenment in a technology's life cycle is reached and implementation of technologies are commencing and need to be understood. AIS Section members also explore information systems issues that are not directly related to technology.

For each new technology development the research potential across all areas of the hype cycle is significant. The combined work of the AIS and SET Sections ensures that the AAA members are kept at the leading edge of research as new technologies move along this cycle.

The above Value Proposition for the SET section of the American Accounting Association was developed in conjunction with the Information Systems Section of the American Accounting Association. Find out further details of this section at http://aaahq.org/infosys/index.cfm.

Interested in technology in accounting, auditing and/or taxation?

Why not join today?

The SET Section welcomes new members who are interested in the potential role and impact of strategic and emerging technologies on all aspects of accounting, auditing and/or taxation. The group particularly welcomes joint membership from members of other AAA sections who are interested in technology aspects of another Section’s focus.

We are a dynamic group that shares a common interest in exploring emerging technologies in the accounting domain, reporting on what we find with academic rigor, discussing it with colleagues and teaching about it to our students. We'd very much welcome those sharing similar interests to join.

To illustrate the diversity of the section, the brief profile details of Section members show how these formal statements are enacted in practice.

Journal

The Journal of Emerging Technologies in Accounting (JETA) is the academic journal of the Strategic and Emerging Technologies Section of the American Accounting Association. The purpose of this section is to improve and facilitate the research, education, and practice of advanced information systems, cutting-edge technologies, and artificial intelligence in the fields of accounting, information technology and management advisory systems. JETA’s Mission is to encourage, support and disseminate the production of a stream of high-quality research focused on emerging technologies and artificial intelligence applied or applicable to a wide set of accounting related problems.

SET Newsletter

Hello SET Section members!

I am currently gathering items for the Summer Section Newsletter, so please let me know if you have any contributions. I would like to share information on:

- Stories and Pictures from the Midyear Meeting

- Calls for Papers

- Teaching Tips or Resources

- Member Profiles (remember I want to emphasize fun items more than CV items)

- Any other topics you think would be interesting to fellow SET members.

Please send your contributions to Jagdish Pathak at jagdish@uwindsor.ca.

A Special Thank You to Our Section Sponsor MMBA!

![]()